Planning in India/5 Year Plans/Niti Aayog

Planning in India Five Year Plans Niti Aayog

Planning in India

Planning is programming for action for a particular period for achieving certain specific progressive developmental goals. In other words, it is a method of achieving economic prosperity by the optimum utilization of the resources of an organization. It is a tool to bridge the gap between reality and objectives of an organization. Also, it is an effort towards attaining self-sufficiency and narrowing the intra and inter-regional disparities and preparing ideal conditions for the development.

The first almost rudimentary idea of economic planning as part of republican justice in India started in 1938 when he was Congress President, Netaji Subhas Bose, with the collaboration of the physicist and mathematician, Meghnad Saha, gave us a glimpse of all that planning for the long term, by an independent and transparent apex, could do for an India of the future. In his presidential address at the Haripura session of the Congress in February 1938, Netaji envisaged “the first task of the Government of Free India” as being the setting up of a “National Planning Commission” in order to address the task of fighting poverty. He created what was, in effect, the nucleus for the future Union Planning Commission in the National Planning Committee under the aegis of the Indian National Congress, with Jawaharlal Nehru as the first Chairman of the Committee.

NEED OF PLANNING

Socio-economic planning has been one of the most noteworthy inventions of the 20th century. Starting with the Soviet experiment in 1928, planning gradually swept over almost two-thirds of the entire world.

1. For developing countries, whether belonging to a democratic or an authoritarian political culture, planning has been considered a prerequisite for balanced socio-economic development and a strategy for making the best possible use of a available natural manpower, and financial as well as infrastructural resources. There are continuing pressures on developing countries to accelerate the speed of development so that the gap between the standard of living of their people and that of the developed countries is reduced at the fastest possible pace and consequently, they also emerge as dignified members of the international community.

2. Even in the developed countries of the west, planning in one form or another, has remained an integral part of their economic system. Only, it is termed “indicative” planning for it is expected to indicate the direction of growth and not to dictate it. Developing countries like China (in late 1970s) and India (in 1990s) started using indicative planning also.

OBJECTIVES OF PLANNING

Indian planning, ever since its inception, has attempted to meet the following objectives of multi-faceted development:

• Securing an increase in national income.

• Accelerating the planned rate of investment to enhance the proportion of actual investment to national income.

• Mitigating the inequalities of income and wealth and regulating the concentration of economic power.

• Increasing the quantum of employment for the maximum possible utilization of manpower.

• Promoting development in agricultural, industrial and other sectors and striving to achieve inter-sectoral development

• Speeding up the development of relatively backward regions and promoting balanced regional development.

• Reducing, in a progressive manner, incidence of poverty by providing food, work and productivity to the people below the poverty-line.

• Modernization of the economy through effecting shifts, in the sectoral composition of production diversification of activities, advancement in technology and institutional innovation.

TYPES OF PLANNING

There have been several experiments in planning in India. The different types of planning that one come across while talking about planning in India are discussed below.

• Indicative Planning

Indicative planning was adopted since 8th five year plan which is driven by liberalization of the Indian economy and the private sector being given a role on par with or more than that of the government in quantitative terms. State would turn its role into a facilitator from that of a controller and regulator.

It was decided that trade and industry would be increasingly freed from government control and that planning in India should become more and more indicative and supportive in nature. In other words, the remodeling of economic growth necessitated recasting the planning model from imperative and directive (‘hard’) to indicative (soft) planning. Since the Government did not contribute the majority of the financial allocation, it had to indicate the policy direction to the corporate sector and encourage them to contribute to plan targets. Government should create the right policy climate – predictable, irreversible and transparent – to help the corporate sector contribute resources for the plan.

Indicative planning is to assist the private sector with information that is essential for its operations regarding priorities and plan targets. Here, the Government and the corporate sector are more or less equal partners and together are responsible for the accomplishment of planning goals. Government, unlike earlier, contributes less than 50% of the financial resources. Government provides the right type of policies and crates the right type of milieu for the private sector-including the foreign sector to contribute to the results.

Indicative planning gives the Government an opportunity to give the private sector encouragement to achieve growth in areas where the country has inherent strengths. It is known to have brought Japan results in shifting towards microelectronics. In France, too indicative planning was in vogue.

Planning Commission would work on building a long-term strategic vision of the future. The concentration would be on anticipating future trends and evolving strategies for competitive international standards. Planning will largely be indicative and the public sector would be gradually withdrawn from areas where no public purpose is served by its presence. The new approach to development will be based on “a re-examination and re-orientation of the role of the government”. The state has to play more of a facilitating role. This point is particularly stressed in the development strategy of the Tenth Five Year Plant (2002-2007).

• Rolling Plan

It was adopted in India in 1962, in the aftermath of Chinese attack on India, in the Defence Ministry in India. Professor Gunnar Mrydal (author of the more famous book ‘Asian Drama’) recommended it for developing countries in his book Indian Economic Planning in Its Broader Setting.

In this type, every year three new plans are made and implemented – annual plan that includes annual budget; three-four-five plan that is changed every year in response to the economic demands; and perspective plan for 10 or 15 years into which the other two plans are dovetailed annually. Rolling plan becomes necessary in circumstances that are fluid.

• Financial Planning

Here, physical targets are set in line with the available financial resources. Mobilization and setting expenditure pattern of financial resources is the focus in this type of planning.

• Physical planning

Here, the output targets are prioritized with inter-sect oral balance. Having set output targets, the finances are raised.

Economic Survey Chapter – 9

Universal Basic Income: A conversation

Universal Basic Income: A conversation(Economic Survey Chapter – 9)

Context

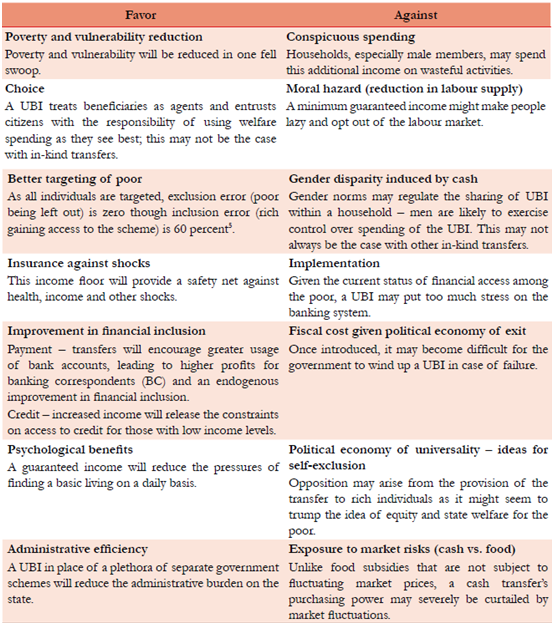

A Universal Basic Income (UBI) is a periodic cash payment unconditionally delivered to all on an individual basis. It is not an entitlement but a right by virtue of being a citizen of a country. UBI is a step towards more equal society as it would promote Social equity, reduce poverty directly, and reduce risks related to unemployment, health etc. by providing a safety net. But, In India’s context the most important benefit would be in terms of addressing misallocation, exclusion and leakages which grapples plethora of schemes run by government to root out poverty and inequality.

Misallocation is due to administrative incapacity and inefficient delivery. Exclusion is a natural consequence of misallocation and Leakages are due to big and complex delivery system. UBI being delivered universally in bank account would address all the three problems. Added benefits would include increase in financial access due to increased volume of transaction which increases profitability of BC model of delivery. There are concerns that UBI would lead to increase in conspicuous consumption and dropout from labour market but studies have found no evidence in this regard.

However, survey chalks out legitimate concerns. The success of UBI hings on success of JAM and still 1/3rd of adults don’t have bank account. The state and Centre need to agree on proportion of funding by each. Finally, taking away all schemes and benefits in lieu of UBI may not be politically feasible. The survey talks about floating the UBI scheme in gradual manner as a way forward.

Misallocation is due to administrative incapacity and inefficient delivery. Exclusion is a natural consequence of misallocation and Leakages are due to big and complex delivery system. UBI being delivered universally in bank account would address all the three problems. Added benefits would include increase in financial access due to increased volume of transaction which increases profitability of BC model of delivery. There are concerns that UBI would lead to increase in conspicuous consumption and dropout from labour market but studies have found no evidence in this regard.

However, survey chalks out legitimate concerns. The success of UBI hings on success of JAM and still 1/3rd of adults don’t have bank account. The state and Centre need to agree on proportion of funding by each. Finally, taking away all schemes and benefits in lieu of UBI may not be politically feasible. The survey talks about floating the UBI scheme in gradual manner as a way forward.

Technical Terms

A. Characteristics of UBI scheme

A basic income has the five following characteristics:

Periodic: it is paid at regular intervals (for example every month), not as a one-off grant.

Cash payment: Allowing those who receive it to decide what they spend it on. It is not, therefore, paid either in kind (such as food or services) or in vouchers dedicated to a specific use.

Individual: It is paid on an individual basis—and not, for instance, to households.

Universal: It is paid to all, without means test.

Unconditional: It is paid without a requirement to work or to demonstrate willingness-to-work.

Periodic: it is paid at regular intervals (for example every month), not as a one-off grant.

Cash payment: Allowing those who receive it to decide what they spend it on. It is not, therefore, paid either in kind (such as food or services) or in vouchers dedicated to a specific use.

Individual: It is paid on an individual basis—and not, for instance, to households.

Universal: It is paid to all, without means test.

Unconditional: It is paid without a requirement to work or to demonstrate willingness-to-work.

B. JAM trinity – An abbreviation for Jan Dhan Yojana, Aadhaar and Mobile number. The government is pinning its hopes on these three modes of identification to deliver direct benefits to India’s poor. Subsidies cost the exchequer quite a bit. Yet, only a part reaches the poor because of intermediaries, leakages, corruption and inefficiencies. This is where the government hopes that the JAM trinity can help. With Aadhaar helping in direct biometric identification of disadvantaged citizens and Jan Dhan bank accounts and mobile phones allowing direct transfers of funds into their accounts, it may be possible to cut out all the intermediaries.

C. Randomize control Trials – In order to test the effect of a variable on a given subject, the subjects are divided into two groups with similar characteristics then the variable is introduced into one group and differences between two groups are studied to know impact of new variable. In UBI case it means taking two similar households and giving UBI to one and observing difference between two groups over a period of time.

D. How UBI does liberate citizens from paternalistic and clientelistic relationships with the state?

Clientelism is a political or social system based on the relation of client to patron with the client giving political or financial support to a patron (as in the form of votes) in exchange for some special privilege or benefit. Ex- voting for a party in exchange for future promised freebies. Because UBI would be Universal this incentive would be killed.

Clientelism is a political or social system based on the relation of client to patron with the client giving political or financial support to a patron (as in the form of votes) in exchange for some special privilege or benefit. Ex- voting for a party in exchange for future promised freebies. Because UBI would be Universal this incentive would be killed.

Paternalism is the interference of a state or an individual with another person, against their will, and defended or motivated by a claim that the person interfered with will be better off or protected from harm. UBI would be in cash so receiver could exercise his discretion to maximize his interests.

Gist of Economic Survey Chapter

Introduction

Despite making remarkable progress in bringing down poverty from about 70 percent at independence to about 22 percent in 2011-12 (Tendulkar Committee), it can safely be said that “wiping every tear from every eye” is about a lot more than being able to imbibe a few calories. It is also about dignity, invulnerability, self-control and freedom, and mental and psychological unburdening. From that perspective, Nehru’s exhortation that “so long as there are tears and suffering, so long our work will not be over” is very much true nearly 70 years after independence.

Idea of a radical option like UBI can be debated to achieve the above objective. UBI requires that every person should have a right to a basic income to cover their needs, just by virtue of being citizens. But there is a need to discuss and debate it pros and cons.

The Conceptual/Philosophical Case for UBI

It has three components: universality, unconditionality, and agency (by providing support in the form of cash transfers to respect, not dictate, recipients’ choices) and shows a radical shift in thinking about social justice and productive economy. It is based on idea that:

• Just society needs to guarantee to each individual a minimum income, and

• Which provides the necessary material foundation for a life with access to basic goods and a life of dignity.

• Which provides the necessary material foundation for a life with access to basic goods and a life of dignity.

It provides various social, economic and administrative benefits to individuals, society and nation.

A. Social justice

• It promotes many of the basic values of a society which respects all individuals as free and equal. It promotes liberty because it is anti-paternalistic; it promotes equality by reducing poverty.

B. Economic benefits

• It promotes efficiency by reducing waste in government transfers.

• System it may simply be the fastest way of reducing poverty.

• UBI is also, paradoxically, more feasible in a country like India, where it can be pegged at relatively low levels of income but still yield immense welfare gains.

• They allow for more non-exploitative bargaining in labour market

• System it may simply be the fastest way of reducing poverty.

• UBI is also, paradoxically, more feasible in a country like India, where it can be pegged at relatively low levels of income but still yield immense welfare gains.

• They allow for more non-exploitative bargaining in labour market

C. Administrative benefits

• A UBI is also practically useful. The circumstances that keep individuals trapped in poverty are varied; the risks they face and the shocks they face also vary. The state is not in the best position to determine which risks should be mitigated and how priorities are to be set and UBI restores decision making with citizens.

• By taking the individual and not the household as the unit of beneficiary, UBI can also enhance agency, especially of women within households.

• In India the case for UBI has been enhanced because of the weakness of existing welfare schemes which are riddled with misallocation, leakages and exclusion of the poor.

However, it is important to recognize that universal basic income will not diminish the need to build state capacity: the state will still have to enhance its capacities to provide a whole range of public goods. UBI is not a substitute for state capacity: it is a way of ensuring that state welfare transfers are more efficient so that the state can concentrate on other public goods.

• By taking the individual and not the household as the unit of beneficiary, UBI can also enhance agency, especially of women within households.

• In India the case for UBI has been enhanced because of the weakness of existing welfare schemes which are riddled with misallocation, leakages and exclusion of the poor.

However, it is important to recognize that universal basic income will not diminish the need to build state capacity: the state will still have to enhance its capacities to provide a whole range of public goods. UBI is not a substitute for state capacity: it is a way of ensuring that state welfare transfers are more efficient so that the state can concentrate on other public goods.

The Conceptual Case Against UBI

From an economic point of view there are three principal and related objections to a universal basic income.

A. The first is whether UBI reduces the incentive to work, which is highly exaggerated because the levels at which universal basic income are likely to be pegged are going to be minimal guarantees at best;

B. The second concern is, should income be detached from employment? But that is already done India in form of rich and privileged accepting non-work related income inherited from their parents. So, receiving a small unearned income as it were, from the state should be economically and morally less problematic than the panoply of “unearned” income our societies allow.

C. The third is a concern out of reciprocity. Should income be unconditional, with no regard to people’s contribution to society? Answer to this is that individuals do contribute to society. UBI in fact will recognize non-wage work by individuals like housewife.

D. Temptation Goods: Would A UBI Promote Vice?

• Detractors of UBI argue that, as a cash transfer programme, this policy will promote conspicuous spending or spending on social evils or temptation goods such as alcohol, tobacco etc.

• But NSSO 2011-12 data shows that these goods form a smaller share of overall budget/consumption as overall consumption increases. This provides an indication that an increase in income from UBI alone will not necessarily lead to an increase in temptation goods consumption.

• Detractors of UBI argue that, as a cash transfer programme, this policy will promote conspicuous spending or spending on social evils or temptation goods such as alcohol, tobacco etc.

• But NSSO 2011-12 data shows that these goods form a smaller share of overall budget/consumption as overall consumption increases. This provides an indication that an increase in income from UBI alone will not necessarily lead to an increase in temptation goods consumption.

E. Moral Hazard: Would A UBI reduce Labour Supply?

• It is argued that free money makes people lazy and they drop out of the labour market because their income levels have increased.

• However controlled trials of government cash transfer programs in 6 developing countries {Honduras, Morocco, Mexico, Philippines, Indonesia and Nicaragua where cash transfer formed between 4 percent (Honduras) and 20 percent (Morocco) of household consumption.} find no significant reduction in labour supply (inside and outside the household) for men or women from the provision of cash transfers. Similar results were obtained from trials in Indian villages from state of Madhya Pradesh.

• However controlled trials of government cash transfer programs in 6 developing countries {Honduras, Morocco, Mexico, Philippines, Indonesia and Nicaragua where cash transfer formed between 4 percent (Honduras) and 20 percent (Morocco) of household consumption.} find no significant reduction in labour supply (inside and outside the household) for men or women from the provision of cash transfers. Similar results were obtained from trials in Indian villages from state of Madhya Pradesh.

F. Another important question why universal basic income and why not targeted direct transfers.

Arguments in Favour and Against UBI

Counter arguments in favor of UBI

Despite all these arguments against UBI, there are various reasons which favor consideration of the idea of universalisation of the schemes, like:

Universalization prevents misallocation and diversion of resources. This can be more understood by analyzing the problems with present welfare schemes.

Large number of schemes:

• India has large number of social welfare schemes. The Budget for 2016-17 indicates that there are about 950 central sector and centrally sponsored sub-schemes in India accounting for about 5 percent of the GDP by budget allocation. Considerable gains could be achieved in terms of bureaucratic costs and time by replacing many of these schemes with a UBI.

Misallocation of resources across districts:

• The poorest areas of the country often obtain a lower share of government resources when compared to their richer counterparts. Under no scheme the poorest districts which have 40% of poor receive 40 percent of the total resources – in fact, for the MDM and SBM, the share is under 25 percent.

• This misallocation results into errors or inclusion of wrong persons and exclusion of genuine poor. An estimate of the exclusion error from 2011-12 suggests that 40 percent of the bottom 40 percent of the population are excluded from the PDS

• This misallocation results into errors or inclusion of wrong persons and exclusion of genuine poor. An estimate of the exclusion error from 2011-12 suggests that 40 percent of the bottom 40 percent of the population are excluded from the PDS

UBI cannot only help in overcoming these above mentioned issues, but will provide other benefits.

A. Improvement in Governance

• Misallocation to districts with less poor will be tackled because resources will be directly transferred to beneficiaries without involving bureaucratic hassles which result into misallocation.

• It will also reduce exclusion errors. Because it is by design universal.

• It will also reduce out of system leakages because JAM platform will be used to directly transfer benefits to beneficiary accounts.

• Misallocation to districts with less poor will be tackled because resources will be directly transferred to beneficiaries without involving bureaucratic hassles which result into misallocation.

• It will also reduce exclusion errors. Because it is by design universal.

• It will also reduce out of system leakages because JAM platform will be used to directly transfer benefits to beneficiary accounts.

B. Insurance against risk

It is found that slightly more than 50 percent of rural households across India face idiosyncratic (individual specific) shocks like bad health, job loss and aggregate shock like natural disaster and natural shock and make them vulnerable to poverty. UBI can prevent such poverty trap.

It is found that slightly more than 50 percent of rural households across India face idiosyncratic (individual specific) shocks like bad health, job loss and aggregate shock like natural disaster and natural shock and make them vulnerable to poverty. UBI can prevent such poverty trap.

C. Psychological benefit

The World Development Report argues that individuals living in poverty have

a) A preoccupation with daily hassles and this results in a depletion of cognitive resources required for important decisions;

b) Low self-image that tends to blunt aspirations;

An assured income could relieve mental space that was used to meet basic daily consumption needs to be used for other activities such as skill acquisition, search for better jobs, etc,and will improve psychological wellbeing.

The World Development Report argues that individuals living in poverty have

a) A preoccupation with daily hassles and this results in a depletion of cognitive resources required for important decisions;

b) Low self-image that tends to blunt aspirations;

An assured income could relieve mental space that was used to meet basic daily consumption needs to be used for other activities such as skill acquisition, search for better jobs, etc,and will improve psychological wellbeing.

D. Improved financial inclusion

Financial inclusion in India has progressed well under PMJDY, with ownership of bank accounts increasing to 2/3rd of adults and active usage to 40%, with only states like Bihar, UP, Jharkhand being laggard. However effective financial inclusion, in terms of active usage is constrained by two factors:

• Physical distance separating people from these bank branches: which is around 4.5 Km from any form of access point (ATM, BC, Bank etc)

• Number of persons per bank, which are very high in high population density like UP, Bihar etc. and greater burden on banks.

UBI can help in improving both these situations.

• UBI will help increasing financial inclusion by increasing bank transactions, increasing business per BC, reducing per unit fixed cost for BCs and thus increasing their numbers.

• At 90% financial inclusion rate with UBI of INR 12,000/person/year and 1% commission for BCs can reduce average distance from banking access point from 4.5Km to 2.5 Km and dramatically improving financial inclusion.

Financial inclusion in India has progressed well under PMJDY, with ownership of bank accounts increasing to 2/3rd of adults and active usage to 40%, with only states like Bihar, UP, Jharkhand being laggard. However effective financial inclusion, in terms of active usage is constrained by two factors:

• Physical distance separating people from these bank branches: which is around 4.5 Km from any form of access point (ATM, BC, Bank etc)

• Number of persons per bank, which are very high in high population density like UP, Bihar etc. and greater burden on banks.

UBI can help in improving both these situations.

• UBI will help increasing financial inclusion by increasing bank transactions, increasing business per BC, reducing per unit fixed cost for BCs and thus increasing their numbers.

• At 90% financial inclusion rate with UBI of INR 12,000/person/year and 1% commission for BCs can reduce average distance from banking access point from 4.5Km to 2.5 Km and dramatically improving financial inclusion.

E. Access to formal credit

Absence of assured income is a constraint for accessing formal credit. UBI can help in overcoming it. Debt and Investment Survey (2013) shows that

• As one moves along the consumption spectrum, the proportion of farmers taking informal loans falls and formal loans take over.

• That there is sudden increase in median loan amounts from zero to sudden increase at 78th percentile (INR 90,000/household/year).

It shows that if everybody’s consumptions could be increased to this level, there might be significant jump in access to formal credit. It also shows that as UBI amount increases more number of households will have access to formal credit, as more number of households will cross 78th percentile limit.

However, it may also occur that income threshold of 78th percentile group an increase and dampening the effect of UBI on releasing credit constraints.

A way forward depending upon the potential costs, fiscal space with governments can be analyzed and possibilities found out.

Absence of assured income is a constraint for accessing formal credit. UBI can help in overcoming it. Debt and Investment Survey (2013) shows that

• As one moves along the consumption spectrum, the proportion of farmers taking informal loans falls and formal loans take over.

• That there is sudden increase in median loan amounts from zero to sudden increase at 78th percentile (INR 90,000/household/year).

It shows that if everybody’s consumptions could be increased to this level, there might be significant jump in access to formal credit. It also shows that as UBI amount increases more number of households will have access to formal credit, as more number of households will cross 78th percentile limit.

However, it may also occur that income threshold of 78th percentile group an increase and dampening the effect of UBI on releasing credit constraints.

A way forward depending upon the potential costs, fiscal space with governments can be analyzed and possibilities found out.

What would be the potential cost of UBI?

The cost of UBI on government finances will depend upon the targets chosen and number of assumption. Based on 2011-12 poverty distribution and their consumption expenditure if a target poverty level of 0.45% is chosen, with UBI of INR 7620 per year (it corresponds to the annual consumption of marginal poor, who is at 0.45% threshold) and 75% coverage the financial cost of UBI will be 4.9% of GDP.

The cost of UBI on government finances will depend upon the targets chosen and number of assumption. Based on 2011-12 poverty distribution and their consumption expenditure if a target poverty level of 0.45% is chosen, with UBI of INR 7620 per year (it corresponds to the annual consumption of marginal poor, who is at 0.45% threshold) and 75% coverage the financial cost of UBI will be 4.9% of GDP.

Fiscal space to Finance a UBI

If we look at the present government welfare programs which are shown in fig., we find that:

• Subsidies for the non-poor/middle class households, equivalent to about 1 percent of GDP.

If we look at the present government welfare programs which are shown in fig., we find that:

• Subsidies for the non-poor/middle class households, equivalent to about 1 percent of GDP.

Fiscal Cost of Existing Central Government Programmes (2015-16)

The middle class subsidies equal to the cost of a UBI of INR 3240 per capita per year provided to all females. This will cost a little over 1 percent of the GDP – or, a little more than the cost of all the middle-class subsidies.

However, taking away subsidies to the middle-class is politically difficult for any government. It is clear that while the fiscal space exists to start a de facto UBI, political and administrative considerations make it difficult to do this without a clearer understanding of its larger economy-wide implications.

However, taking away subsidies to the middle-class is politically difficult for any government. It is clear that while the fiscal space exists to start a de facto UBI, political and administrative considerations make it difficult to do this without a clearer understanding of its larger economy-wide implications.

Guiding Principle for Setting up a UBI

A. De jure universality, de facto quasi-universality

Using automatic exclusion criterion like:

• Ownership of key assets such as AC, automobiles

• Adopt a give up scheme

• Public display of UBI list, this would ‘name and shame’ the rich who choose to avail themselves of UBI.

• Self-targeting: under this Develop a system where beneficiaries regularly verify them in order to avail themselves of their UBI – the assumption here is that the rich, whose opportunity cost of time is higher, would not find it worth their while to go through this process and the poor would self-target into the scheme. However, this run counters to the objective of JAM trinity.

A. De jure universality, de facto quasi-universality

Using automatic exclusion criterion like:

• Ownership of key assets such as AC, automobiles

• Adopt a give up scheme

• Public display of UBI list, this would ‘name and shame’ the rich who choose to avail themselves of UBI.

• Self-targeting: under this Develop a system where beneficiaries regularly verify them in order to avail themselves of their UBI – the assumption here is that the rich, whose opportunity cost of time is higher, would not find it worth their while to go through this process and the poor would self-target into the scheme. However, this run counters to the objective of JAM trinity.

B. Gradualism

A guiding principle is gradualism: the UBI must be embraced in a deliberate, phased manner. A key advantage of phasing would be that it allows reform to occur incrementally – weighing the costs and benefits at every step. This can be done in following ways:

A guiding principle is gradualism: the UBI must be embraced in a deliberate, phased manner. A key advantage of phasing would be that it allows reform to occur incrementally – weighing the costs and benefits at every step. This can be done in following ways:

C. Choice to persuade and to establish the principle of replacement, not additionally

• Under this UBI is offered as a choice to beneficiaries of existing programs. Apart from having the normal advantages of cost reduction, giving choice to beneficiaries it will give them greater negotiating power with administrators, which will force latter to improve their performance.

• However it will have its own disadvantages of enforcing current problems with targeting, continues with the problem of misallocation with richer districts getting more, does not solve the problem of wrong exclusion and inclusion and will be cumbersome to administer.

• Under this UBI is offered as a choice to beneficiaries of existing programs. Apart from having the normal advantages of cost reduction, giving choice to beneficiaries it will give them greater negotiating power with administrators, which will force latter to improve their performance.

• However it will have its own disadvantages of enforcing current problems with targeting, continues with the problem of misallocation with richer districts getting more, does not solve the problem of wrong exclusion and inclusion and will be cumbersome to administer.

D. UBI for women

• It is worth considering because women suffer worse prospects in almost every aspect of their daily lives – employment opportunities, education, health or financial inclusion. Simultaneously, the higher social benefits and the multi-generational impact of improved development outcomes for women.

• A UBI for women can, therefore, not only reduce the fiscal cost of providing a UBI (to about half) but have large multiplier effects on the household. It will increase their bargaining power; reduce concerns of money being splurged on conspicuous goods and by factoring in children in household higher UBI can be provided to women.

However this has three problems of counting number of children, parents may go for more children and identification & phasing out of boys after they reach 18 years of age.

• It is worth considering because women suffer worse prospects in almost every aspect of their daily lives – employment opportunities, education, health or financial inclusion. Simultaneously, the higher social benefits and the multi-generational impact of improved development outcomes for women.

• A UBI for women can, therefore, not only reduce the fiscal cost of providing a UBI (to about half) but have large multiplier effects on the household. It will increase their bargaining power; reduce concerns of money being splurged on conspicuous goods and by factoring in children in household higher UBI can be provided to women.

However this has three problems of counting number of children, parents may go for more children and identification & phasing out of boys after they reach 18 years of age.

E. Universalize across groups:

Certain groups like widows, old age, divyang etc can be included under UBI net under phase-1 because these groups are easily identifiable. However this may suffer from less access to bank accounts and not part of JAM trinity.

Certain groups like widows, old age, divyang etc can be included under UBI net under phase-1 because these groups are easily identifiable. However this may suffer from less access to bank accounts and not part of JAM trinity.

F. UBI in urban areas:

Urban areas have proper banking infrastructure and as poor are less dependent on state for sustenance, a disruptive step like UBI will not be that tricky in these areas.

Urban areas have proper banking infrastructure and as poor are less dependent on state for sustenance, a disruptive step like UBI will not be that tricky in these areas.

Prerequisites for UBI

A. JAM

Financial inclusion is very necessary for success of UBI. In India considerable ground has been covered for JAM preparedness but still a lot needs to be done.

• 1/3 of population is still without bank account and most of them belong to vulnerable social groups like SC, ST, disabled etc.

• Though 26.5 cr. Jan Dhan accounts have been opened, but linkages with Aadhar lags in J&K and north east states.

• Though 1 billion Aadhar cards have issued, but there are instances of authentication failure in states like Jharkhand (49% failure rates) and Rajasthan (having 37% failure rates), which results into exclusion.

It is not clear, whether UBI will certainly result into fewer leakages. Given the amount of cash that will flow through the system under the UBI and the fungible nature of money, one could imagine a perverse equilibrium where the UBI results in greater capture by corrupt actors.

This, once again, reiterates the role of a transparent and safe financial architecture that is accessible to all – the success of the UBI hinges on the success of JAM.

A. JAM

Financial inclusion is very necessary for success of UBI. In India considerable ground has been covered for JAM preparedness but still a lot needs to be done.

• 1/3 of population is still without bank account and most of them belong to vulnerable social groups like SC, ST, disabled etc.

• Though 26.5 cr. Jan Dhan accounts have been opened, but linkages with Aadhar lags in J&K and north east states.

• Though 1 billion Aadhar cards have issued, but there are instances of authentication failure in states like Jharkhand (49% failure rates) and Rajasthan (having 37% failure rates), which results into exclusion.

It is not clear, whether UBI will certainly result into fewer leakages. Given the amount of cash that will flow through the system under the UBI and the fungible nature of money, one could imagine a perverse equilibrium where the UBI results in greater capture by corrupt actors.

This, once again, reiterates the role of a transparent and safe financial architecture that is accessible to all – the success of the UBI hinges on the success of JAM.

B. Center-state negotiations

UBI amount, sharing between center and state will be very crucial for success of UBI. All these will require complex negotiations between federal stakeholders.

Initially, a minimum UBI can be funded wholly by the center. The center can then adopt a matching grant system wherein for every rupee spent in providing a UBI by the state, the center matches it.

UBI amount, sharing between center and state will be very crucial for success of UBI. All these will require complex negotiations between federal stakeholders.

Initially, a minimum UBI can be funded wholly by the center. The center can then adopt a matching grant system wherein for every rupee spent in providing a UBI by the state, the center matches it.

Conclusion

UBI is a powerful idea whose time even if not ripe for implementation is ripe for serious discussion. UBI can help in wiping tears form all eyes, which Mahatma Gandhi dreamed of, but it would also have serious consequences in form of

• Uncompensated reward harming responsibility and effort;

• Effect on macro-economic stability of country; and

• Recognizing exit problem in India, UBI may become another add-on government programme,which would have come to mind of Mahatma Gandhi.

UBI is a powerful idea whose time even if not ripe for implementation is ripe for serious discussion. UBI can help in wiping tears form all eyes, which Mahatma Gandhi dreamed of, but it would also have serious consequences in form of

• Uncompensated reward harming responsibility and effort;

• Effect on macro-economic stability of country; and

• Recognizing exit problem in India, UBI may become another add-on government programme,which would have come to mind of Mahatma Gandhi.

Supplementary Reading

Left-wing views – Socialist and left-wing economists and sociologists have advocated a form of Universal Basic Income (UBI) as a means for distributing the economic profits of publicly owned enterprises to benefit the entire population (also referred to as a social dividend), where the basic income payment represents the return to each citizen on the capital owned by society. Basic income as a project for reforming capitalism into a socialist system by empowering labor in relation to capital, granting labor greater bargaining power with employers in labor markets, which can gradually de-commodify labor by decoupling work from income. Some thinkers view an income guarantee would benefit all workers by liberating them from the anxiety that results from the “tyranny of wage slavery” and provide opportunities for people to pursue different occupations and develop untapped potentials for creativity.

Right Wing View – For thinkers on the right, the UBI. seems like a simpler, and more libertarian, alternative to the thicket of anti-poverty and social-welfare programs. For their part, right-wing advocates of the UBI view it as a streamlined replacement for complicated welfare payments. For this reason, Milton Friedman, an economist known for his laissez-faire beliefs, wanted to replace all welfare with a simpler system that combined a guaranteed minimum income.

Debate in Europe – European Parliament’s committee on Legal affairs (JURI) adopted a report on “Civil law rules on robotics” which considers the legal and economic consequences of the rise of robots and artificial intelligence devices. The report argues that development of robotics and AI may result in a large part of the work now done by humans being taken over by robots, so raising concerns about the future of employment and the viability of social security systems, creating the potential for increased inequality in the distribution of wealth and influence. To cope with those consequences, the report makes a strong call for basic income.

On the other hand, in June 2016, Swiss voters overwhelmingly rejected a proposal to guarantee an income to Switzerland’s residents, whether or not they are employed, an idea that has also been raised in other countries amid an intensifying debate over wealth disparities and dwindling employment opportunities.

Switzerland was the first country to vote on such a universal basic income plan, but other countries and cities either have been considering the idea or have started trial programs. Finland has introduce a pilot program for a random sample of about 10,000 adults who will each receive a monthly handout of 550 euros, about $625. The intent is to turn the two-year trial into a national plan if it proves successful.

Views from Experts : The Indian Statistical Institute hosted its 12th Annual Conference on Economic Growth and Development (ACEGD) on December 19-21, 2016. ACEGD’s plenary sessions included a 90-minute panel on universal basic income and its relevance for India.

This conference included a panel on UBI, featuring five economists: Debraj Ray (New York University), Kalle (Karl Ove) Moene (University of Oslo), Rajiv Sethi (Columbia University), Himanshu (Jawaharlal Nehru University), and Amarjeet Sinha (Government of Bihar).

Ray and Moene have jointly developed a proposal for what they call a “universal basic share” (UBS) in India. Like a UBI, a UBS would provide each citizen with regular unconditional cash transfers of an equal amount. However, in contrast to most UBI proposals, a UBS fixes the amount of these transfers to a fraction of the GDP rather than a specific monetary amount. Ray and Moene recommend that India dedicate 12% of its GDP to the provision of a UBS. They calculate that, at present, this would provide each adult citizen with a basic income approximately equal to the country’s poverty line.

The last two panelists, Himanshu and Sinha, argue that India should prioritize public spending on universal basic services, rather than simply distributing cash to individuals. About UBI, Himanshu states that the question is not whether it should be adopted, but why and when. While allowing that UBI is a good idea in principle, he maintains that it is not yet time to introduce such a policy in India, given that many in the country lack clean water, access to education, and other essential public goods. Sinha, expanding on Himanshu’s thesis, stresses that “we should not lose sight of the need to craft credible public systems” — and worries that a UBI would divert money and attention from necessary improvements of education, health, housing, and public infrastructure.

Right Wing View – For thinkers on the right, the UBI. seems like a simpler, and more libertarian, alternative to the thicket of anti-poverty and social-welfare programs. For their part, right-wing advocates of the UBI view it as a streamlined replacement for complicated welfare payments. For this reason, Milton Friedman, an economist known for his laissez-faire beliefs, wanted to replace all welfare with a simpler system that combined a guaranteed minimum income.

Debate in Europe – European Parliament’s committee on Legal affairs (JURI) adopted a report on “Civil law rules on robotics” which considers the legal and economic consequences of the rise of robots and artificial intelligence devices. The report argues that development of robotics and AI may result in a large part of the work now done by humans being taken over by robots, so raising concerns about the future of employment and the viability of social security systems, creating the potential for increased inequality in the distribution of wealth and influence. To cope with those consequences, the report makes a strong call for basic income.

On the other hand, in June 2016, Swiss voters overwhelmingly rejected a proposal to guarantee an income to Switzerland’s residents, whether or not they are employed, an idea that has also been raised in other countries amid an intensifying debate over wealth disparities and dwindling employment opportunities.

Switzerland was the first country to vote on such a universal basic income plan, but other countries and cities either have been considering the idea or have started trial programs. Finland has introduce a pilot program for a random sample of about 10,000 adults who will each receive a monthly handout of 550 euros, about $625. The intent is to turn the two-year trial into a national plan if it proves successful.

Views from Experts : The Indian Statistical Institute hosted its 12th Annual Conference on Economic Growth and Development (ACEGD) on December 19-21, 2016. ACEGD’s plenary sessions included a 90-minute panel on universal basic income and its relevance for India.

This conference included a panel on UBI, featuring five economists: Debraj Ray (New York University), Kalle (Karl Ove) Moene (University of Oslo), Rajiv Sethi (Columbia University), Himanshu (Jawaharlal Nehru University), and Amarjeet Sinha (Government of Bihar).

Ray and Moene have jointly developed a proposal for what they call a “universal basic share” (UBS) in India. Like a UBI, a UBS would provide each citizen with regular unconditional cash transfers of an equal amount. However, in contrast to most UBI proposals, a UBS fixes the amount of these transfers to a fraction of the GDP rather than a specific monetary amount. Ray and Moene recommend that India dedicate 12% of its GDP to the provision of a UBS. They calculate that, at present, this would provide each adult citizen with a basic income approximately equal to the country’s poverty line.

The last two panelists, Himanshu and Sinha, argue that India should prioritize public spending on universal basic services, rather than simply distributing cash to individuals. About UBI, Himanshu states that the question is not whether it should be adopted, but why and when. While allowing that UBI is a good idea in principle, he maintains that it is not yet time to introduce such a policy in India, given that many in the country lack clean water, access to education, and other essential public goods. Sinha, expanding on Himanshu’s thesis, stresses that “we should not lose sight of the need to craft credible public systems” — and worries that a UBI would divert money and attention from necessary improvements of education, health, housing, and public infrastructure.

Start Up India Scheme

Start Up India Scheme

• Government of India has launched the Start-Up India initiative which aimed at promoting entrepreneurial culture in the country. Start-up India Action Plan was unveiled providing a slew of incentives for the youth to become job creators rather than job seekers.

• According to the government notification, an entity will be identified as a startup.

a) Till up to five years from the date of incorporation.

b) If its turnover does not exceed 25 crores in the last five financial years.

c) It is working towards innovation, development, deployment, and commercialization of new products, processes, or services driven by technology or intellectual property.

b) If its turnover does not exceed 25 crores in the last five financial years.

c) It is working towards innovation, development, deployment, and commercialization of new products, processes, or services driven by technology or intellectual property.

• Start-up India Action Plan highlights are:

a) Compliance Regime based on Self-Certification: There are provisions of self certification to comply with various labour and environment laws such as Contract Labour (Regulation and Abolition) Act, 1970 or Air (Prevention & Control of Pollution) Act, 1981 etc. It has been done to reduce the regulatory burden on Startups thereby allowing them to focus on their core business and keep compliance cost low.

b) Mobile App & Portal: The government has proposed to create a single window web portal or Mobile App for purpose of registration of start-ups, tracking status of registration, Filing compliances for various clearances/approvals, applying for various schemes or collaborating with various Startup ecosystem partners etc.

c) Fast-tracking Patent Examination at Lower Costs: For effective implementation of the scheme, a panel of “facilitators” shall be empanelled by the Controller General of Patents, Designs and Trademarks (CGPDTM), who shall also regulate their conduct and functions. The government will bear entire facilitation costs and startups have to pay only statutory fees for patent registration. Startups shall be provided an 80% rebate in filing of patents as compared to other companies.

d) Faster Exit for Startups: In terms of the Insolvency and Bankruptcy Bill 2015 (IBB) which has been tabled in Lok Sabha, Startups with simple debt structures or those meeting such criteria as may be specified may be wound up within a period of 90 days from making of an application for winding up on a fast track basis.

e) Funding: Under Start-up India scheme, government will set up a fund with an initial corpus of Rs 2500 Cr and total corpus of Rs 10000 Cr for next 4 years. The Fund will be in the nature of Fund of Funds, which means that it will not invest directly into Startups, but shall participate in the capital of SEBI registered Venture Funds.

f) Tax Benefits: Start-ups shall be exempted from income tax for a period of first 3 years.

g) Atal Innovation Mission (AIM) and SETU: The AIM has launched with Start-up India scheme. It has two main functions that are as follows:

b) Mobile App & Portal: The government has proposed to create a single window web portal or Mobile App for purpose of registration of start-ups, tracking status of registration, Filing compliances for various clearances/approvals, applying for various schemes or collaborating with various Startup ecosystem partners etc.

c) Fast-tracking Patent Examination at Lower Costs: For effective implementation of the scheme, a panel of “facilitators” shall be empanelled by the Controller General of Patents, Designs and Trademarks (CGPDTM), who shall also regulate their conduct and functions. The government will bear entire facilitation costs and startups have to pay only statutory fees for patent registration. Startups shall be provided an 80% rebate in filing of patents as compared to other companies.

d) Faster Exit for Startups: In terms of the Insolvency and Bankruptcy Bill 2015 (IBB) which has been tabled in Lok Sabha, Startups with simple debt structures or those meeting such criteria as may be specified may be wound up within a period of 90 days from making of an application for winding up on a fast track basis.

e) Funding: Under Start-up India scheme, government will set up a fund with an initial corpus of Rs 2500 Cr and total corpus of Rs 10000 Cr for next 4 years. The Fund will be in the nature of Fund of Funds, which means that it will not invest directly into Startups, but shall participate in the capital of SEBI registered Venture Funds.

f) Tax Benefits: Start-ups shall be exempted from income tax for a period of first 3 years.

g) Atal Innovation Mission (AIM) and SETU: The AIM has launched with Start-up India scheme. It has two main functions that are as follows:

– Entrepreneurship promotion through Self-Employment and Talent Utilization (SETU), wherein innovators would be supported and mentored to become successful entrepreneurs. Establishment of 500 Tinkering Labs, Pre-incubation training, Strengthening of incubation and Seed funding are some examples of entrepreneurship promotion.

– Innovation promotion: to provide a platform where innovative ideas are generated such as Institution of Innovation Awards (3 per state/UT) and 3 National level awards etc.

– Innovation promotion: to provide a platform where innovative ideas are generated such as Institution of Innovation Awards (3 per state/UT) and 3 National level awards etc.

h) Govt will create innovation or Start-up centres at national institutes such as IITs, NITs or IIITs with various facilities like incubation, etc.

Stand Up India Scheme

Stand Up India Scheme

• The Govt of India has recently approved the “Stand up India Scheme” to promote entrepreneurship among SC/ST and Women entrepreneurs.

• The Scheme is intended to facilitate at least two such projects per bank branch, on an average one for each category of entrepreneur.

• The scheme aims to benefit at least 2.5 lakh women and SC/ST entrepreneurs. The scheme has target of 2.5 lakh loan approvals within 36 months.

• The Stand Up India Scheme provides for:

• The Scheme is intended to facilitate at least two such projects per bank branch, on an average one for each category of entrepreneur.

• The scheme aims to benefit at least 2.5 lakh women and SC/ST entrepreneurs. The scheme has target of 2.5 lakh loan approvals within 36 months.

• The Stand Up India Scheme provides for:

a) Refinance window through Small Industries Development Bank of India (SIDBI) with an initial amount of Rs. 10,000 crore.

b) Creation of a credit guarantee mechanism through the National Credit Guarantee Trustee Company (NCGTC).

c) Handholding support for borrowers both at the pre loan stage and during operations. This would include increasing their familiarity with factoring services, registration with online platforms and e-market places as well as sessions on best practices and problem solving.

b) Creation of a credit guarantee mechanism through the National Credit Guarantee Trustee Company (NCGTC).

c) Handholding support for borrowers both at the pre loan stage and during operations. This would include increasing their familiarity with factoring services, registration with online platforms and e-market places as well as sessions on best practices and problem solving.

• The overall intent of the approval is to leverage the institutional credit structure to reach out to these under-served sectors of the population by facilitating bank loans repayable up to 7 years and between Rs. 10 lakh to Rs. 100 lakh for greenfield enterprises in the non farm sector set up by such SC, ST and Women borrowers.

• The loan under the scheme would be appropriately secured and backed by a credit guarantee through a credit guarantee scheme for which Department of Financial Services would be the settler and National Credit Guarantee Trustee Company Ltd. (NCGTC) would be the operating agency.

• Margin money of the composite loan would be up to 25%. Convergence with state schemes is expected to reduce the actual requirement of margin money for a number of borrowers. o Over a period of time, it is proposed that a credit history of the borrower be built up through Credit Bureaus.

• The loan under the scheme would be appropriately secured and backed by a credit guarantee through a credit guarantee scheme for which Department of Financial Services would be the settler and National Credit Guarantee Trustee Company Ltd. (NCGTC) would be the operating agency.

• Margin money of the composite loan would be up to 25%. Convergence with state schemes is expected to reduce the actual requirement of margin money for a number of borrowers. o Over a period of time, it is proposed that a credit history of the borrower be built up through Credit Bureaus.

Terminologies Associated with Start Up Funds

Terminologies Associated with Start Up Funds

• Seed capital/Seeding:

It is a form of securities offering in which an investor invests capital in exchange for an equity stake in the company. Seed capital is the initial capital used when starting a business, often coming from the founders’ personal assets, friends or family, for covering initial operating expenses and attracting venture capitalists. This type of funding is often obtained in exchange for an equity stake in the enterprise, although with less formal contractual overhead than standard equity financing. Because banks and venture capital investors view seed capital as an “at risk” investment by the promoters of a new venture, capital providers may wait until a business is more established before making larger investments of venture capital funding.

• Seed Stock:

An investment security that is based on shares of a publicly traded, agriculture-based company is involved in plant research and development. A seed stock is any stock that represents a company that researches and produces seeds for planting crops and develops new seed products to increase farmers’ yields or otherwise improve seed performance.

• Angle investors:

They are an affluent individual who provides capital for a business start-up, usually in exchange for convertible debt or ownership equity. A small but increasing number of angel investors invest online through equity crowd funding or organize themselves into angel groups or angel networks to share research and pool their investment capital, as well as to provide advice to their portfolio companies.

• Incubators:

They work with startups to develop entrepreneurial skills such as building a business around an idea, creating and testing a prototype and understanding the market. Incubator programmes can be relatively long-term – over a year.

• Accelerators:

They offer usually shorter and more intense programmes to hone in on the business model, the market opportunity and the product.

• Co-working:

These spaces are shared offices that typically have open space and offer desk space as well as other facilities such as administrative help or services such as couriers. In addition, there may be formal or informal networks of mentors or entrepreneurs based at the co-working space. India’s largest cities have a number of co-working spaces.

No comments:

Post a Comment